Building Private Transfers on Ethereum with Plasma

In a recent post, we built a shielded pool for private stablecoin transfers on Ethereum L1. The approach works: KYC-gated entry, UTXO commitments, dual-key architecture for selective disclosure. But every transfer writes new commitments and nullifiers to the chain. The pool contract’s state grows with every transaction, and every state transition requires on-chain ZK proof verification.

Rather than iterating on the shielded pool, we explored a different approach.

Plasma and Zero-Knowledge Proofs

Plasma was proposed in 2017 as a scaling solution where side chains would post only block headers to Ethereum L1. Several variants followed (Plasma MVP, Plasma Cash), but none succeeded. The core problem was data availability: if the operator withheld transaction data, users could not prove their balances to exit safely. Optimistic rollups solved this by posting full transaction data on-chain. Validiums added validity proofs but moved data availability off-chain to a Data Availability Committee. Both approaches effectively replaced plasma for general computation.

Advances in zero-knowledge cryptography mitigate plasma’s core drawback. If users can prove their balances cryptographically, the chain does not need to store transaction data, and neither does any external committee. The old exit game, challenge-response disputes over withheld data, becomes unnecessary.

In this design, a block builder collects transaction hashes, aggregates them into a Merkle tree, and posts the block root along with an aggregated BLS signature on-chain. The builder never sees transaction contents, only salted hashes. Users generate ZK proofs of their balances locally and hold them client-side. If the builder disappears, users still have everything they need to prove their balances and withdraw their funds.

For institutions, this changes the operating model. Transaction contents (amounts, recipients, balances) never touch the chain or any third-party server in plaintext. The operator has no access to transaction data and cannot be compelled to produce it. Deposits can be gated by KYC attestation proofs, the same mechanism from the shielded pool PoC, so only verified participants enter the system. Viewing keys give regulators read-only access to a specific participant’s full transaction history without exposing other users. The dual-key architecture (spending key for transfers, viewing key for audits) maps directly to how banks separate operational authority from audit access.

The tradeoffs are different from the shielded pool. On-chain costs drop significantly since the chain only stores block roots and signatures. Privacy against public observers is stronger because transfer details are never published, but client-side proof generation is computationally intensive, the anonymity set depends on the deployment model, and the infrastructure stack (block builders, store vaults, provers) introduces new operational dependencies.

We built a proof-of-concept on Intmax2, a ZK-plasma protocol that implements this model with recursive proofs via Plonky2. The specification covers every protocol flow and data structure in detail.

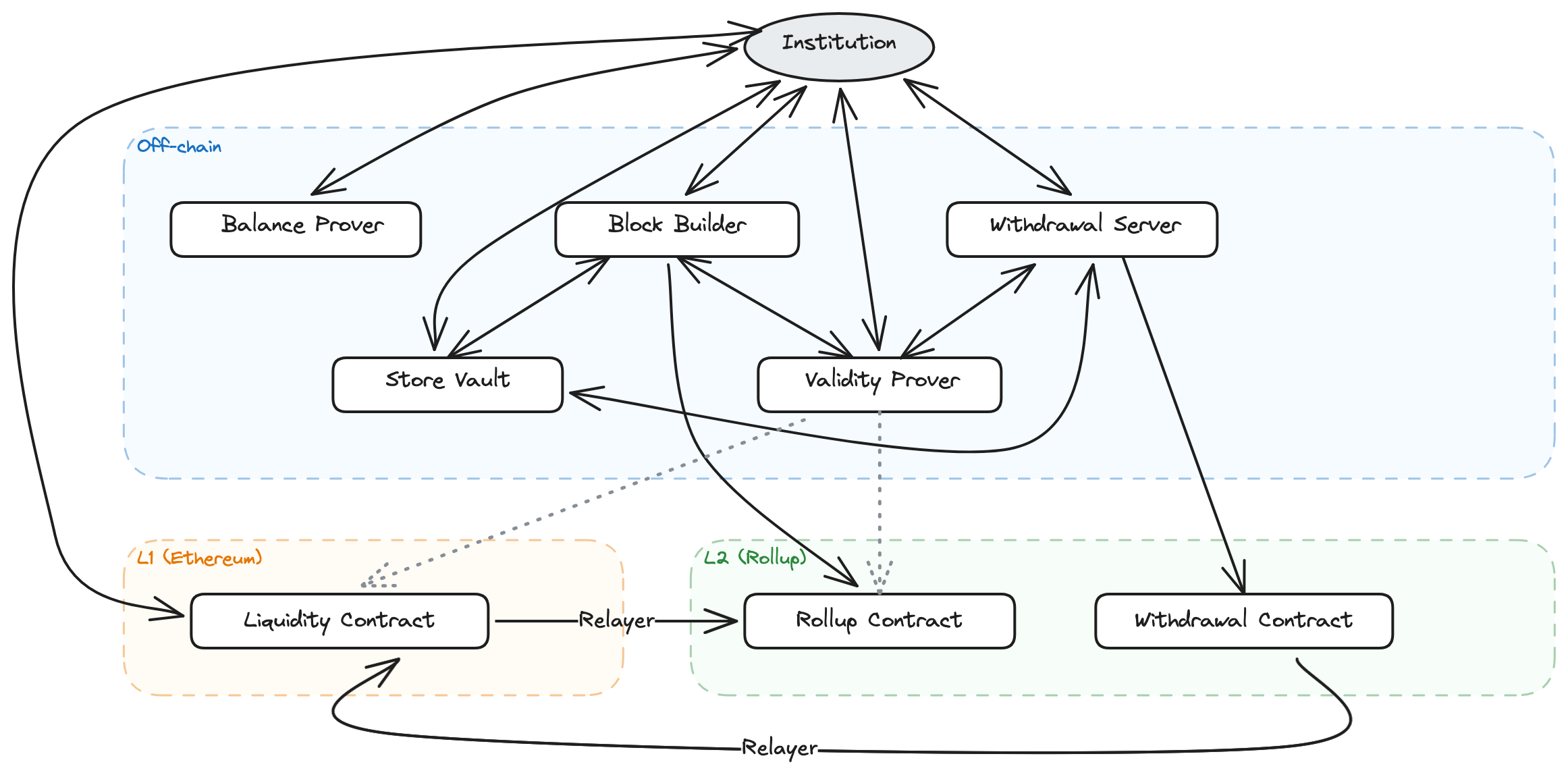

Architecture

- Institution: holds keys locally, initiates deposits, transfers, and withdrawals

- Store Vault: encrypted off-chain storage where senders publish transaction data for recipients to retrieve

- Balance Prover: generates ZK proofs for client operations (spend, send, receive, withdraw)

- Validity Prover: monitors on-chain events, maintains Merkle trees, generates validity proofs for block state transitions

- Withdrawal Server: validates withdrawal requests, aggregates proofs, relays to the Withdrawal contract

- Block Builder: collects transaction hashes, aggregates BLS signatures, posts blocks to the Rollup contract

- Liquidity Contract (L1): holds deposited tokens, relays deposits to L2, releases tokens on withdrawal claims

- Rollup Contract (L2): stores block commitments, manages the deposit Merkle tree

- Withdrawal Contract (L2): verifies withdrawal proofs, relays claims to L1

- Relayer: Cross-chain messaging service

Each component is pluggable: the proof backend, storage layer, and contract interaction can be replaced independently.

How Private Transfers Work

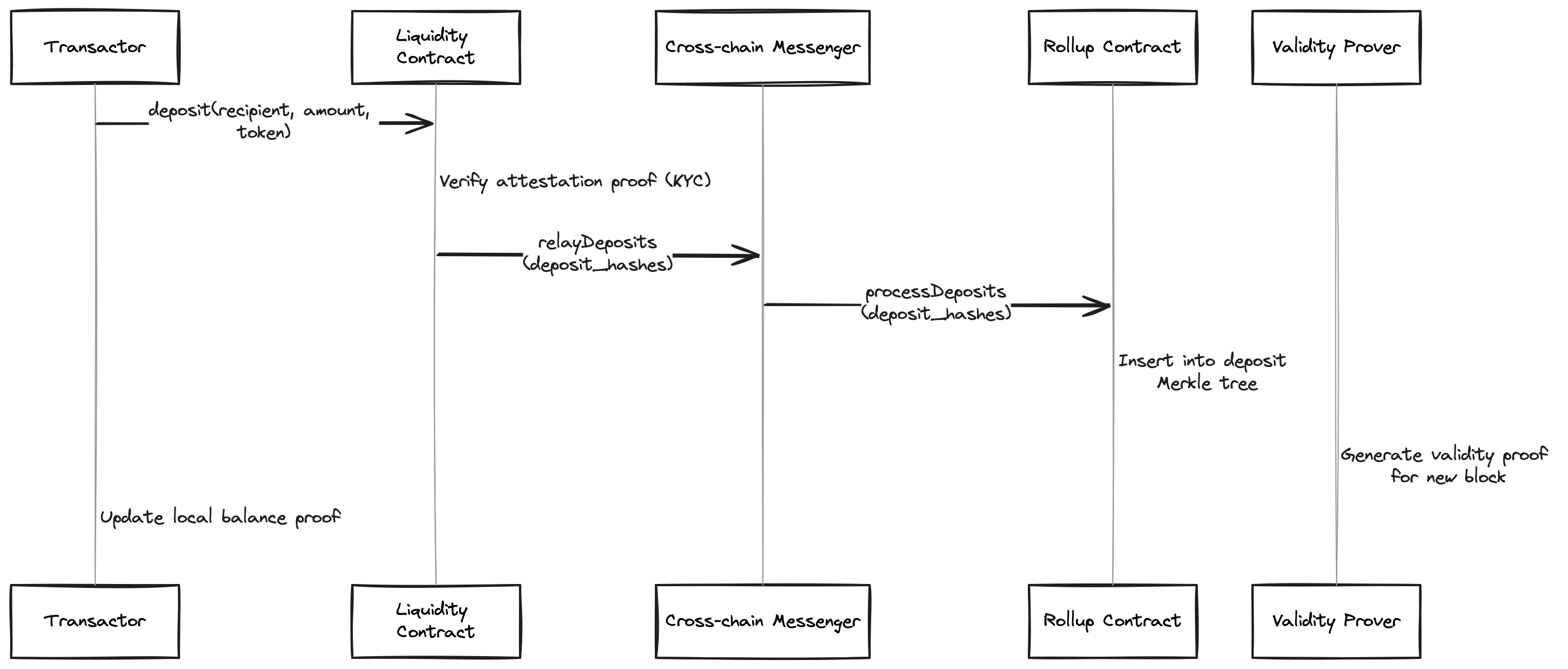

Deposits

Deposits convert public ERC-20 tokens into a private balance on the plasma chain. The user locks tokens in a Liquidity contract on L1. The contract relays deposit data to the Rollup contract on the L2 via a cross-chain messenger. The Rollup contract inserts the deposit into its Merkle tree, and the validity prover asynchronously generates a proof for the new block state. The user polls until the deposit is confirmed, then updates their local balance proof.

In the target architecture, deposits are gated by an attestation registry: a ZK proof of Merkle inclusion in an on-chain KYC attestation tree, identical in concept to the shielded pool’s approach. The attestation registry from the shielded pool PoC can be reused here with minimal modification; the core mechanism is the same.

The attestation proof is zero-knowledge: the on-chain verifier learns only that the depositor holds a valid, non-expired KYC attestation. It does not learn which attestation leaf was used, which compliance authority issued it, or when the attestation was granted. An observer sees that someone deposited a known amount of a known token, but cannot determine who deposited it or which compliance authority verified them.

Deposit flow: tokens lock on L1, relay to the Rollup contract on L2, and the user updates their local balance proof after the validity prover confirms the block.

Private Transfers

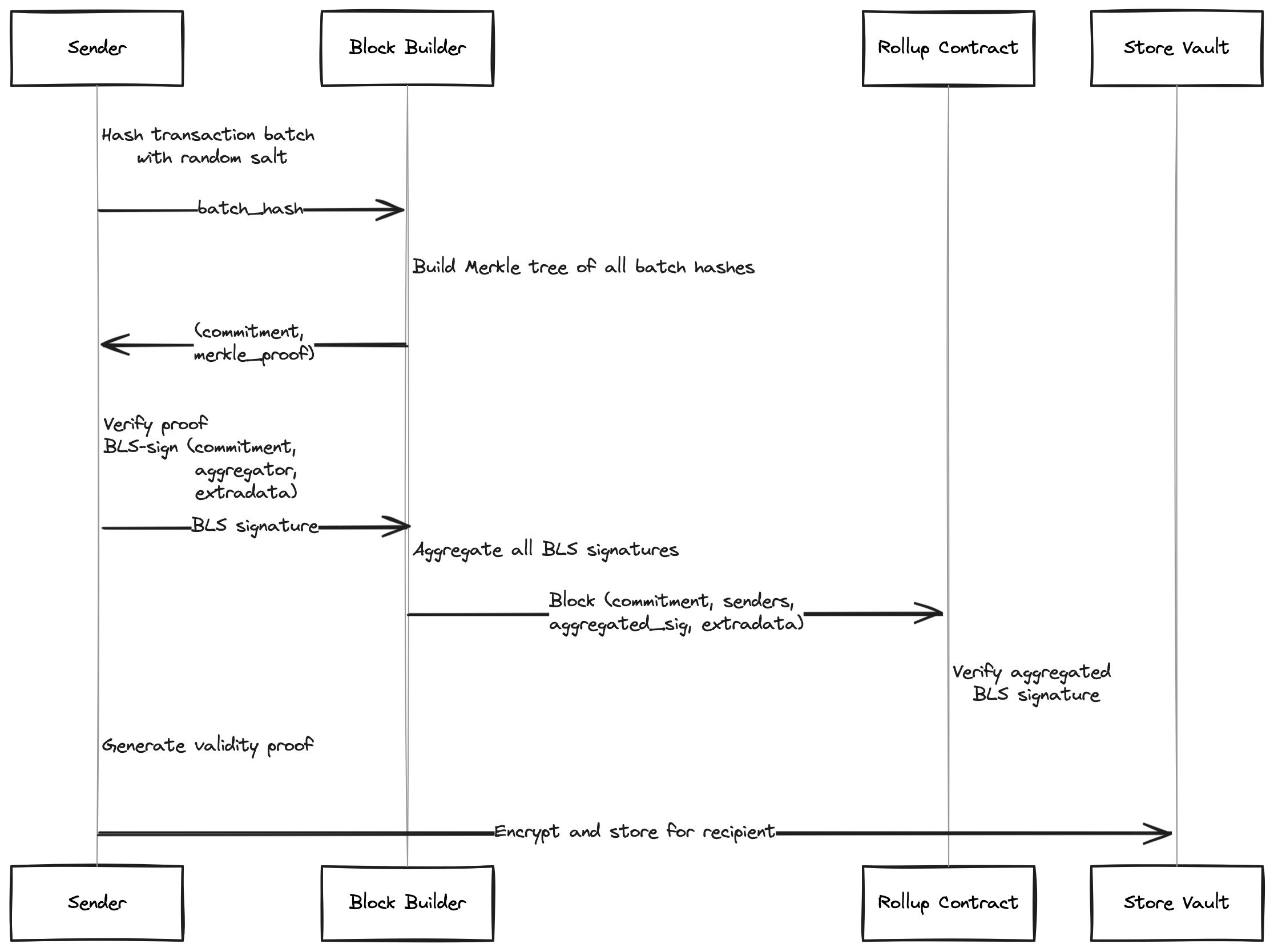

This is the core operation. The sender constructs a transaction batch (a mapping of recipients to amounts), hashes it with a random salt, and sends only the hash to a block builder. The builder collects hashes from multiple senders, constructs a Merkle tree, and sends each sender the tree root with their inclusion proof. Each sender verifies their proof and BLS-signs the commitment along with the aggregator’s identity and replay-protection metadata. The builder aggregates all signatures into a single compact signature and posts the block to the Rollup contract.

The block builder never sees transaction contents, only salted hashes. It cannot determine who is paying whom or how much.

After the block is posted, the sender generates a recursive ZK validity proof attesting to sufficient balance, encrypts it with the transaction details, and stores it in the store vault. The recipient retrieves and decrypts the data using their viewing key.

The zero-knowledge property here is precise: the recipient learns only the sender’s identity, the amount, and that the sender had sufficient balance at the time of the transfer. They learn nothing about the sender’s total balance, other recipients in the sender’s transaction batch, or what any other sender in the block was doing. The sender list (public keys) for each block is visible on-chain, so observers can see who participated as senders, but not what they sent or to whom. Repeated participation across blocks also reveals activity frequency: an observer can track how often a public key appears as a sender, even without knowing transfer contents or recipients.

Transfer flow: the block builder only sees salted hashes. After the block is posted, the sender encrypts the transaction details for the recipient via the store vault.

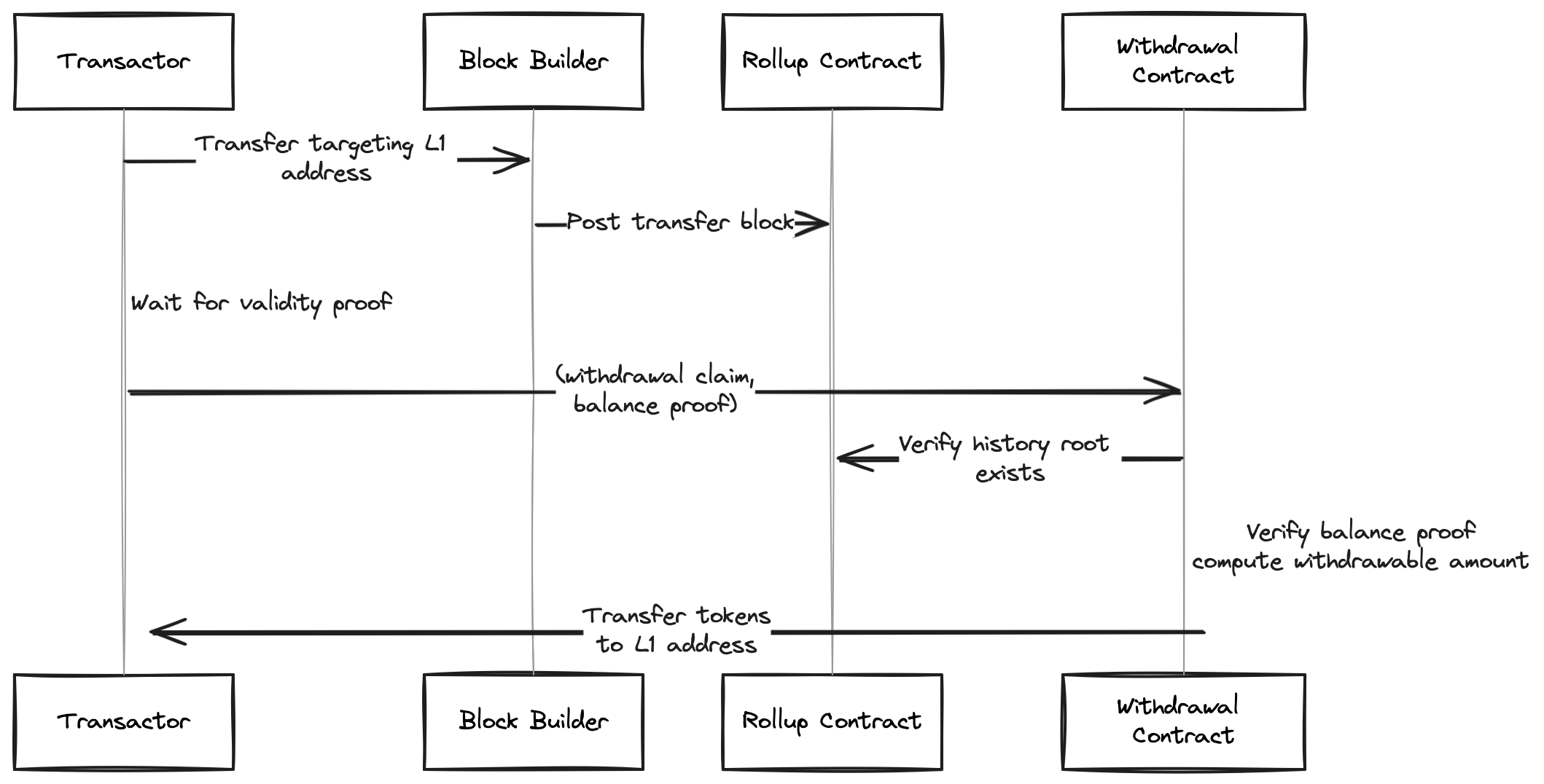

Withdrawals

Withdrawals convert a private plasma balance back to public L1 tokens. The user constructs a transfer targeting an L1 address, which signals withdrawal intent and goes through the normal transfer protocol. Once the block is proven by the validity prover, the user submits a withdrawal claim to the Withdrawal contract with a ZK balance proof. The contract verifies the proof, deducts any previously withdrawn amounts, and transfers tokens to the L1 address.

Withdrawal flow: the user proves their balance via a ZK proof and claims tokens on L1.

Self-Hosted vs. Public Network

Intmax2 supports two deployment models: a private instance where the institution controls all infrastructure, or the public Intmax network where the protocol team operates block builders and store vaults.

| Dimension | Private Instance | Public Network |

|---|---|---|

| Compliance control | Full; institution sets attestation rules, KYC policy, revocation procedures | Shared; subject to Intmax’s compliance framework |

| Anonymity set | Limited to institution’s users | Broader, shared across all network participants |

| Infrastructure cost | High; block builders, store vaults, validity prover | None; protocol team operates everything |

| Metadata exposure | Controlled; institution runs its own store vaults | Store vault operator sees access patterns (no PIR) |

| Protocol upgrades | Institution controls upgrade cadence | Subject to Intmax governance decisions |

For a pilot or proof-of-concept, the public network minimizes operational overhead. For production deployments with regulatory obligations, where the institution needs to control who can transact, what compliance rules apply, and how data is stored, a private instance provides that control at the cost of running and maintaining the full infrastructure stack.

Compliance Properties

The design maps each privacy mechanism to a specific regulatory obligation:

- Attestation-gated entry. Deposits require a ZK proof of KYC verification before funds enter the system, supporting obligations under the Bank Secrecy Act and MiCA’s stablecoin provisions.

- Selective disclosure. Viewing keys give regulators read-only access to a specific participant’s full transaction history without exposing other users, supporting GDPR’s data minimization principle.

- Separated authority. The dual-key architecture (spending key for transfers, viewing key for audits) maps directly to how banks separate operational authority from audit access.

- Travel Rule support. The store vault’s encrypted data model enables counterparty information sharing between institutions as required by FATF Recommendation 16, without exposing that data to public observers.

Threat Model

- Public observer: sees block commitments, sender public keys, and deposit/withdrawal amounts; cannot link senders to recipients or determine transfer amounts within a block. Repeated participation across blocks reveals activity frequency.

- Malicious block builder: can delay or censor transactions but cannot steal funds or read transaction contents. Users can switch builders or run their own.

- Compromised store vault: operator learns access patterns (who queries when) but cannot decrypt data.

- Compromised viewing key: leaks one user’s full history without granting spending authority.

The specification documents mitigations for each adversary class in detail.

Limitations

This PoC demonstrates the full deposit-transfer-withdraw flow against a live testnet. It is not production-ready. The following limitations are real constraints for institutions evaluating this approach.

No Private Information Retrieval on store vaults. The store vault holds encrypted transaction data, but the server sees access patterns: which users query which topics, and when. No PIR is employed. An adversary controlling the store vault can correlate access timing with on-chain events. On a private instance, the institution controls the vault, limiting exposure. On the public network, this is a meaningful privacy gap. Mitigation: run your own store vault, or await PIR integration.

Compliance tradeoff on the public network. Using the public Intmax network means the institution does not control who else transacts on the system. The institution must comply with whatever AML framework Intmax defines, rather than enforcing its own. For institutions with strict counterparty screening or jurisdictional requirements, this creates regulatory friction. A private instance avoids this entirely.

Protocol maturity. Intmax2 is a live protocol, not a battle-tested production system. The cryptographic primitives (Plonky2, BLS aggregation, Poseidon hashing) are well-studied, and the protocol’s fund safety property has been formally verified in Lean. But the full stack, including block builders, store vaults, validity provers, and deposit/withdrawal contracts, has not undergone years of adversarial testing. Smart contract audits remain a prerequisite for institutional deployment.

Centralization in current deployment. Block builders and store vaults are operated by the Intmax team. The protocol is designed for permissionless operation, and anyone can run a block builder, but the ecosystem has not decentralized yet. A single operator failure or policy change could disrupt the network. This mirrors early rollup centralization: a known issue with a clear path forward, not yet realized.

Client-side proof generation. Recursive ZK proof generation (Plonky2) is computationally intensive. The SDK targets desktop and server environments. For institutional back-office systems this is acceptable; for customer-facing mobile wallets it may not be.

Viewing key compromise. A compromised viewing key leaks all historical transaction data for that user, with no rotation mechanism. Same limitation as the shielded pool approach.

None of these are fundamental blockers. Each has a known mitigation path, but they are real constraints for any institution evaluating this approach today.

Related Work

The idea of replacing Plasma’s fraud proofs with SNARKs has been explored since 2018. Plasma Snapp proposed a fully SNARK-verified Plasma chain, eliminating exit games and confirmation signatures entirely. Quark-Gluon Plasma took an account-based approach, using zkSNARKs to prove state transitions over sparse Merkle trees. NOCUST-ZKP extended commit-chains with zkSNARK-verified operator state, reaching production in 2019. Matter Labs contributed non-inclusion zkSNARKs for compressing Plasma Cash history proofs via RSA accumulators. These proposals predated the proving infrastructure needed to make client-side ZK practical, but they established the core insight that Intmax2 and similar protocols now build on.

What Comes Next

Private transfers are one layer of an institutional payment pipeline. Upcoming posts will tackle the pieces that connect transfers to real-world payment infrastructure: messaging standards like ISO 20022 for structured payment data, off-chain coordination for settlement finality, and the full end-to-end pipeline from payment initiation to settlement confirmation.

On the proving layer, PlasmaBlind is an emerging alternative that uses folding-scheme-based IVC rather than Plonky2’s recursive SNARKs for the balance proof pipeline. Folding schemes reduce client-side proving costs, which could make generating balance proofs on mobile and browser clients more practical. It is under active R&D by PSE.

The implementation is open source. The specification covers every protocol flow, data structure, and security consideration in detail. The use case and approach documents on the IPTF Map provide additional context. Pull requests are welcome.